Posted By: laz

Changing "LookBack" produces completely different results? - 02/19/19 16:38

Hello everybody, I am currently testing an example from the following link:

https://robotwealth.com/getting-started-neural-networks-algorithmic-trading/

I adjusted the script

and was surprised by the results.

But if you change "LookBack" from 100 to 200, the result changes drastically:

The Trades / Signals (Output) of the Perceptron are also very different.

Why is that?

https://robotwealth.com/getting-started-neural-networks-algorithmic-trading/

I adjusted the script

Code:

function run() {

set(RULES|PEEK|OPENEND|TESTNOW|PLOTNOW|LOGFILE);

StartDate = 2014;

EndDate = 2016;

BarPeriod = 60;

LookBack = 100;

NumWFOCycles = 5;

DataSplit = 80;

if(Train) Hedge = 2;

MaxBars = slider(2,0,0,100000,"MaxBars","MaxBars");

PlotWidth = slider(3,1500,1500,10000,"PlotWidth","PlotWidth");

asset("EURUSD");

Spread = Commission = Slippage = RollLong = RollShort = 0;

vars Close = series(priceClose());

var Sig1 = scale(ATR(10)-ATR(50), 100);

var Sig2 = (Close[0]-Close[1])/Close[1];

var Sig3 = (Close[0]-Close[5])/Close[5];

var Sig4 = (Close[0]-Close[10])/Close[10];

var ObL = -1;

var ObS = -1;

if(priceClose(-5) - priceClose(0) > 20*PIP) ObL = 1;

if(priceClose(-5) - priceClose(0) < -20*PIP) ObS = 1;

LifeTime = 5;

var l = adviseLong (PERCEPTRON+BALANCED, ObL , Sig1, Sig2, Sig3, Sig4);

var s = adviseShort(PERCEPTRON+BALANCED, ObS , Sig1, Sig2, Sig3, Sig4);

if(!Train) {

if(l > 0 and s < 0) reverseLong(1); else

if(s > 0 and l < 0) reverseShort(1);

}

ObL = ifelse(ObL>0,ObL,0);

ObS = ifelse(ObS>0,ObS,0);

l = ifelse(l>0,l,0);

s = ifelse(s>0,s,0);

plot("ObL", ObL, NEW, GREEN);

plot("ObS",-ObS, 0, RED);

plot("l", l, NEW, GREEN);

plot("s",-s, 0, RED);

}

and was surprised by the results.

Quote:

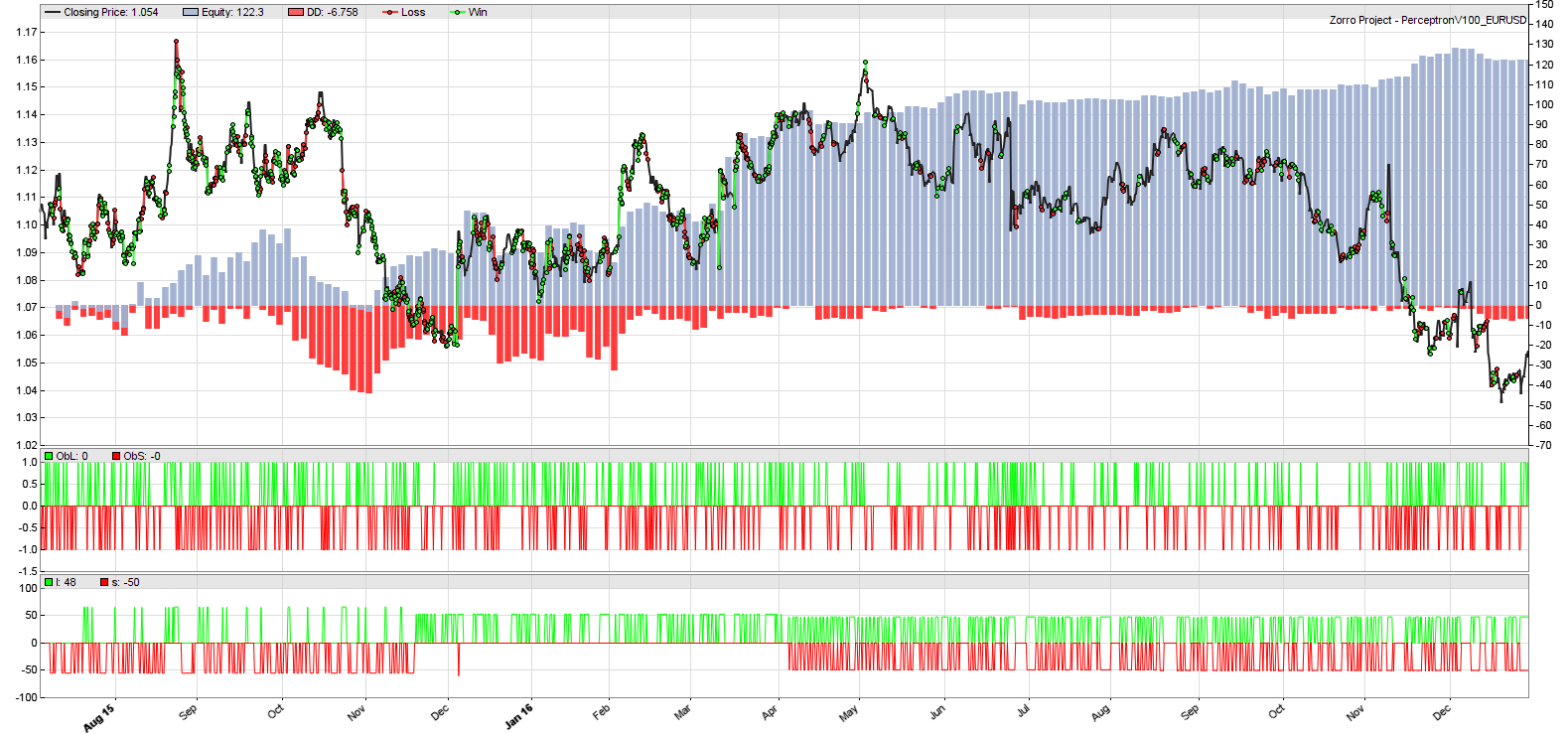

WFA Test PerceptronV100 EURUSD

Simulated account AssetsFix

Bar period 1 hour (avg 86 min)

Simulation period 2014-01-08..2016-12-30 (18208 bars)

Test period 2015-07-06..2016-12-30 (9105 bars)

Lookback period 100 bars (4 days)

WFO test cycles 4 x 2276 bars (19 weeks)

Training cycles 5 x 9103 bars (78 weeks)

Montecarlo cycles 200

Simulation mode Realistic (slippage 0.0 sec)

Avg bar 9.0 pips range

Spread 0.0 pips (roll 0.00/0.00)

Contracts per lot 1000.0

Gross win/loss 627$ / -505$ (+1393p)

Average profit 82.24$/year, 6.85$/month, 0.32$/day

Max drawdown -46.39$ 37.9% (MAE -47.85$ 39.1%)

Total down time 88% (TAE 31%)

Max down time 7 weeks from Dec 2015

Max open margin 2.56$

Max open risk 10.24$

Trade volume 575122$ (386798$/year)

Transaction costs 0$ spr, 0$ slp, 0$ rol

Capital required 68.46$

Number of trades 593 (399/year, 8/week, 2/day)

Percent winning 51.3%

Max win/loss 30.52$ / -11.34$

Avg trade profit 0.21$ 2.3p (+23.5p / -19.9p)

Avg trade slippage 0$ 0.0p (+0.0p / -0.0p)

Avg trade bars 5 (+5 / -5)

Max trade bars 7 (7 hours)

Time in market 39%

Max open trades 1

Max loss streak 8 (uncorrelated 9)

Annual return 120%

Profit factor 1.24 (PRR 1.11)

Sharpe ratio 1.44

Kelly criterion 1.73

R2 coefficient 0.864

Ulcer index 12.6%

Simulated account AssetsFix

Bar period 1 hour (avg 86 min)

Simulation period 2014-01-08..2016-12-30 (18208 bars)

Test period 2015-07-06..2016-12-30 (9105 bars)

Lookback period 100 bars (4 days)

WFO test cycles 4 x 2276 bars (19 weeks)

Training cycles 5 x 9103 bars (78 weeks)

Montecarlo cycles 200

Simulation mode Realistic (slippage 0.0 sec)

Avg bar 9.0 pips range

Spread 0.0 pips (roll 0.00/0.00)

Contracts per lot 1000.0

Gross win/loss 627$ / -505$ (+1393p)

Average profit 82.24$/year, 6.85$/month, 0.32$/day

Max drawdown -46.39$ 37.9% (MAE -47.85$ 39.1%)

Total down time 88% (TAE 31%)

Max down time 7 weeks from Dec 2015

Max open margin 2.56$

Max open risk 10.24$

Trade volume 575122$ (386798$/year)

Transaction costs 0$ spr, 0$ slp, 0$ rol

Capital required 68.46$

Number of trades 593 (399/year, 8/week, 2/day)

Percent winning 51.3%

Max win/loss 30.52$ / -11.34$

Avg trade profit 0.21$ 2.3p (+23.5p / -19.9p)

Avg trade slippage 0$ 0.0p (+0.0p / -0.0p)

Avg trade bars 5 (+5 / -5)

Max trade bars 7 (7 hours)

Time in market 39%

Max open trades 1

Max loss streak 8 (uncorrelated 9)

Annual return 120%

Profit factor 1.24 (PRR 1.11)

Sharpe ratio 1.44

Kelly criterion 1.73

R2 coefficient 0.864

Ulcer index 12.6%

But if you change "LookBack" from 100 to 200, the result changes drastically:

Quote:

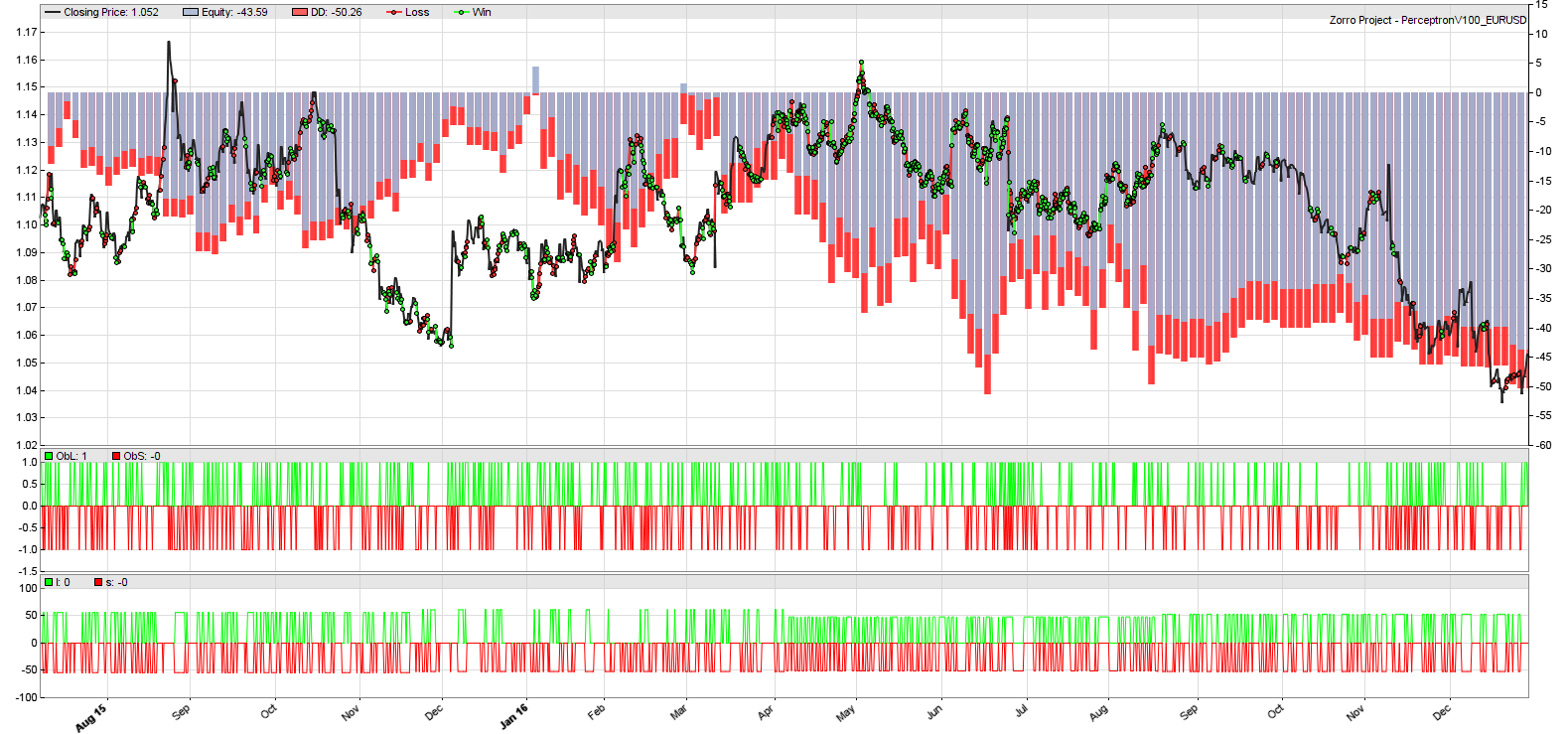

WFA Test PerceptronV100 EURUSD

Simulated account AssetsFix

Bar period 1 hour (avg 86 min)

Simulation period 2014-01-14..2016-12-30 (18108 bars)

Test period 2015-07-08..2016-12-30 (9055 bars)

Lookback period 200 bars (12 days)

WFO test cycles 4 x 2263 bars (19 weeks)

Training cycles 5 x 9053 bars (78 weeks)

Simulation mode Realistic (slippage 0.0 sec)

Avg bar 9.1 pips range

Spread 0.0 pips (roll 0.00/0.00)

Contracts per lot 1000.0

Gross win/loss 551$ / -594$ (-497p)

Average profit -29.43$/year, -2.45$/month, -0.11$/day

Max drawdown -60.19$ -138.1% (MAE -64.42$ -147.8%)

Total down time 99% (TAE 39%)

Max down time 23 weeks from Jan 2016

Max open margin 2.54$

Max open risk 10.17$

Trade volume 759622$ (512850$/year)

Transaction costs 0$ spr, 0$ slp, 0$ rol

Capital required 88.20$

Number of trades 777 (525/year, 11/week, 3/day)

Percent winning 50.1%

Max win/loss 10.58$ / -14.76$

Avg trade profit -0.0561$ -0.6p (+16.1p / -17.4p)

Avg trade slippage 0$ 0.0p (+0.0p / -0.0p)

Avg trade bars 5 (+5 / -5)

Max trade bars 7 (7 hours)

Time in market 46%

Max open trades 1

Max loss streak 7 (uncorrelated 10)

Annual return -33%

Profit factor 0.93 (PRR 0.84)

Sharpe ratio -0.54

Kelly criterion -0.89

R2 coefficient 0.555

Ulcer index 100.0%

Simulated account AssetsFix

Bar period 1 hour (avg 86 min)

Simulation period 2014-01-14..2016-12-30 (18108 bars)

Test period 2015-07-08..2016-12-30 (9055 bars)

Lookback period 200 bars (12 days)

WFO test cycles 4 x 2263 bars (19 weeks)

Training cycles 5 x 9053 bars (78 weeks)

Simulation mode Realistic (slippage 0.0 sec)

Avg bar 9.1 pips range

Spread 0.0 pips (roll 0.00/0.00)

Contracts per lot 1000.0

Gross win/loss 551$ / -594$ (-497p)

Average profit -29.43$/year, -2.45$/month, -0.11$/day

Max drawdown -60.19$ -138.1% (MAE -64.42$ -147.8%)

Total down time 99% (TAE 39%)

Max down time 23 weeks from Jan 2016

Max open margin 2.54$

Max open risk 10.17$

Trade volume 759622$ (512850$/year)

Transaction costs 0$ spr, 0$ slp, 0$ rol

Capital required 88.20$

Number of trades 777 (525/year, 11/week, 3/day)

Percent winning 50.1%

Max win/loss 10.58$ / -14.76$

Avg trade profit -0.0561$ -0.6p (+16.1p / -17.4p)

Avg trade slippage 0$ 0.0p (+0.0p / -0.0p)

Avg trade bars 5 (+5 / -5)

Max trade bars 7 (7 hours)

Time in market 46%

Max open trades 1

Max loss streak 7 (uncorrelated 10)

Annual return -33%

Profit factor 0.93 (PRR 0.84)

Sharpe ratio -0.54

Kelly criterion -0.89

R2 coefficient 0.555

Ulcer index 100.0%

The Trades / Signals (Output) of the Perceptron are also very different.

Why is that?